Heat Check Time: an important 4th quarter earnings season

The fourth quarter reporting period is the reporting period that feels like it never ends. That is because year-end accounting is enmeshed with the quarterly reports. Things have already gotten rolling last week when the big banks reported their results, but we won't be putting a lid on this particular reporting period until early March.

The stock market has a chance to heat up if the results and, importantly, the guidance impress. If they don't, then it may be a long, cold stretch for a market that is also wrestling with rising interest rates.

Full, Rich, and Fiery

It isn't breaking new ground to suggest the earnings multiple for the market cap-weighted S&P 500 is high on a historical basis. Currently, it sits at 21.6x forward 12-month earnings, down from 22.5 seen in early December but still high relative to the 10-yr average of 18.1, according to FactSet.

We have discussed before, however, that the earnings multiple for the equal-weighted S&P 500 is less demanding on an absolute and relative basis. It sits at 16.4x forward twelve-month earnings versus a 10-yr average of 16.5x. On this basis, the market is not overvalued.

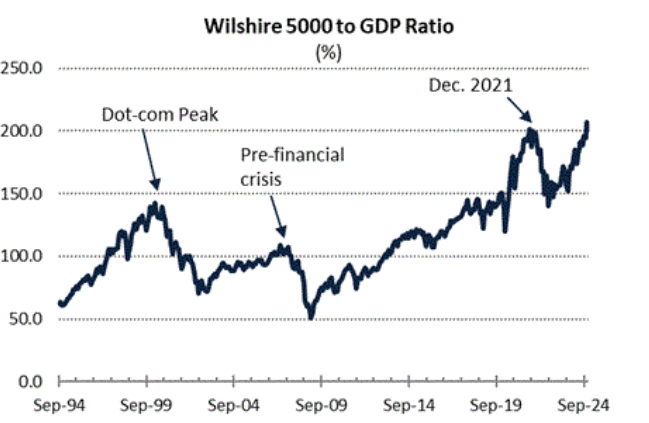

Sill, someone like Warren Buffett might contend that "the stock market" is overvalued in a big way when looking at the ratio of the Wilshire 5000 market capitalization to nominal GDP.

That happens to be known as the "Buffett Indicator" after he observed in a 2001 Forbes Magazine interview that, "If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200%-as it did in 1999 and a part of 2000-you are playing with fire." Today, it sits at 202%.

One's view of the stock market's valuation, then, may just boil down to one's risk tolerance, yet we will say this: the stock market's valuation ranges from full to rich to fiery, partly because a lot of good earnings news has been priced into it -- not just past earnings news but future earnings news that is expected to be even better.

That is why there is a lot riding on the fourth quarter reports to start the new year. Companies will be providing a lot of qualitative and quantitative guidance for the first quarter and year ahead that will validate, or invalidate, the market's optimistic outlook.

Riding High

According to FactSet, the fourth quarter blended earnings growth rate is 11.7%. That is down from 14.5% on September 30, yet it would still mark the highest year-over-year growth rate since the fourth quarter of 2021.

But wait, it gets better. The first quarter earnings growth rate is projected to be 11.8% and for calendar year 2025 it is projected to be 14.8%. So, one can see expectations are riding high into 2025.

For the fourth quarter, the financial sector is expected to deliver the strongest growth (39.5%) followed by the communication services (20.8%), information technology (13.9%), consumer discretionary (12.8%), and utilities (12.5%) sectors.

The remaining sectors are projected to trail the S&P 500 growth rate. Four sectors are expected to have negative year-over-year earnings growth: consumer staples (-1.6%), industrials (-3.7%), materials (-4.6%), and energy (-26.4%).

The overall growth rate will be in a state of flux as the results roll in. BlackRock (BLK), BNY Mellon (BK), Citigroup (C), Goldman Sachs (GS), JPMorgan Chase (JPM), and Wells Fargo (WFC) will get that ball rolling on January 15.

With a new administration pushing deregulation and more market-friendly tax policy, the qualitative guidance out of the big banks should sound pretty encouraging, although they will have to work to temper concerns about the impact of rising interest rates on loan demand and debt issuance/refinancing.

Meanwhile, multinational companies are going to have to temper concerns about the impact of the strengthening dollar while companies in general are going to have to temper concerns about the impact of potential tariffs.

The latter won't be easy to do since new tariffs haven't been enacted, and there is no telling how penal they will be or the countries/products at which they will be aimed, although it is fair to say that China is tops on the new administration's tariff list.

CY25 earnings estimate have been reined in since September, roughly coinciding with the dollar's ascendance.

What It All Means

There will be a lot of time to get a fix on the calendar year 2025 earnings line given the extended nature of the fourth quarter earnings reporting period. The cast of that line will happen as companies report their year-end results and analysts fish for information that moves their earnings models.

Clearly for a market trading at best with a full valuation, it won't want the earnings growth line reeled in. It would presumably be content to see that line remain fixed and even happier if it is let out some more to catch additional earnings growth.

That isn't getting easier with the dollar strengthening and interest rates rising. The upcoming, and extended, fourth quarter reporting period will be an important tell for a stock market that has been priced for nothing but good earnings news.